How to eliminate medical bills

Medical bill debt elimination is very straight forward once you have the right methodology. Debt filtration is the only way to remove collection debt. In fact, most hospitals simply send your bills to collection automatically. If your insurance fails to pay the hospital in a timely fashion, they will simply send that bill to a debt collector even though the insurance pays them eventually. There is so much fraud in debt collections that the government has created laws to reduce the effect of collections on your credit report. Nearly 1-in-5 households in the United States has reported having some form of overdue medical debt. Patients and their families are contacted by debt collectors about medical bills more than any other type of debt, and it commonly results in negative information appearing on credit records. In fact, in 2021, 43 million people had allegedly unpaid medical bills on their credit reports.

Congress, federal agencies, and others have taken steps to respond to the medical debt crisis confronting millions of families. Congress passed the No Surprises Act to help protect Americans from certain unexpected medical bills, including surprise medical bills for emergency services from out-of-network providers. In addition, the CFPB told debt collectors and consumer credit reporting companies that they can’t collect, furnish, or report any invalid medical debt.

The three nationwide credit reporting companies – Equifax, Experian, and TransUnion – also removed all paid medical debts from consumer credit reports and those less than a year old. They have also taken steps to remove all medical collections under $500. This last step went into effect on April 11, 2023, and with this change, it’s estimated that roughly half of those with medical debt on their reports will have it removed from their credit history.

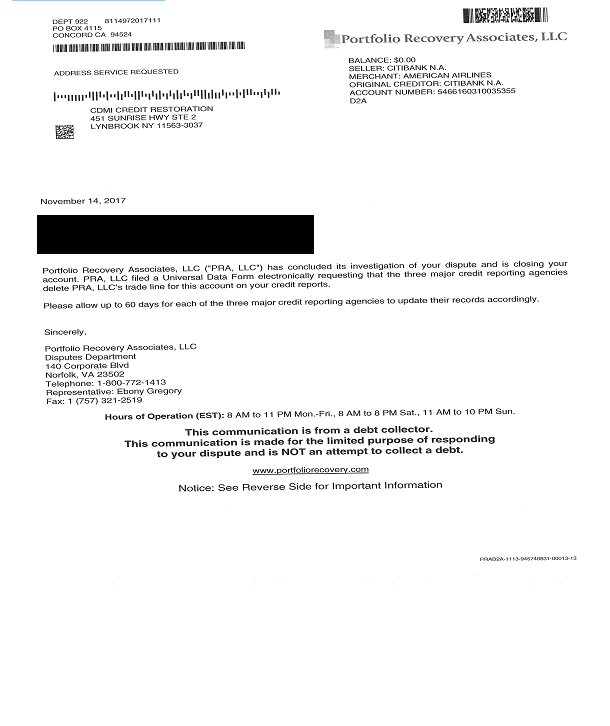

If you’re one of the millions of Americans with overdue medical bills, you may be able to take steps to ensure this information no longer affects your credit, including your access to employment and housing by using proper debt filtration techniques provided by our company. See example.

“(a) There is abundant evidence of the use of abusive, deceptive, and unfair debt collection practices by many debt collectors. Abusive debt collection practices contribute to the number of personal bankruptcies, to marital instability, to the loss of jobs, and to invasions of individual privacy.”

Unfortunately, a lot of law firms are really debt collectors, so this statement includes them. What Congress is trying to tell you is that you are filing bankruptcy for debt that you don’t really have to pay because the government has already given you a debt filter to get rid of these bad debts (Cancelation and Forgiveness remember). The reason that your attorney probably recommended bankruptcy is because they did not study credit and debt law in law school. In fact, very little attention is spent on these subjects. The reason is because it is considered to be a bad business model by lawyers to focus on a client base that is broke and has bad credit. So to your disservice most attorneys recommend bankruptcy because it is easy to file and is very lucrative for them and your “purported creditors”. See example.